Civil Action No. 00-CV-12485-RCL______________________________________ ) Reginald H. Howe, ) Plaintiff, ) ) v. ) ) Bank for International Settlements, ) Alan Greenspan, ) William J. McDonough, ) J.P. Morgan & Co. Inc., ) Chase Manhattan Corp., ) Citigroup, Inc., ) Goldman Sachs Group, Inc., ) Deutsche Bank AG and ) Lawrence H. Summers, ) Secretary of the Treasury, ) Defendants. ) ______________________________________)COMPLAINT I. Jurisdiction 1. This is a complaint for damages and injunctive relief arising out of manipulative activities in the gold market from 1994 to the present time orchestrated by government officials acting outside the scope of their legal or constitutional authority and certain large bullion banks active in the over-the-counter gold derivatives markets and on the Commodities Exchange ("COMEX") in New York. The complaint alleges horizontal price fixing in violation of Section 1 of the Sherman Act, securities fraud in violation of Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934 ("Exchange Act"), common law fraud and breach of fiduciary duty by the directors of the Bank for International Settlements with regard to holders of its American issue, and violations of the Constitution by federal officials acting under color of federal law but wholly outside the scope of their legal or constitutional authority. Subject matter jurisdiction of the federal claims is based on 15 U.S.C. s. 15(a) (antitrust) and s. 78aa (violations of the Exchange Act), 28 U.S.C. s. 1331 (federal question), s. 1337 (commerce and antitrust) and s. 2201 (declaratory relief), and 12 U.S.C. s. 632 (international banking and financial transactions). Supplemental jurisdiction of the common law claims is based on 28 U.S.C. s. 1367.

II. Parties, Venue and Standing 2. The plaintiff, Reginald H. Howe, is an American citizen, residing currently and at all times material hereto at 49 Tyler Road, Belmont, Massachusetts 02478. He is suing in his individual capacity as: (1) the duly registered holder of six shares of the American issue of the Bank for International Settlements; and (2) the holder of 1200 depositary shares of Gold-Denominated Preferred Stock, Series II, of Freeport-McMoran Copper & Gold, Inc. The plaintiff is the proprietor of The Golden Sextant (www.goldensextant.com), an internationally recognized website containing commentaries, essays and analyses relating to gold, and a member of Golden Sextant Advisors LLC. The plaintiff has engaged in research and analysis on gold derivatives, which are instruments such as forward contracts, futures, options and swaps whose value is tied to -- or derived from -- the price of gold, and in this connection has uncovered considerable evidence of their use to manipulate gold prices.

3. While the plaintiff has not assigned any part of this action to others and retains full control thereof, he has received and expects to continue to receive support, both financial and informational, from the Gold Anti-Trust Action Committee Inc. ("GATA"), a civil rights and educational organization formed under Delaware law in January 1999 to expose manipulation of the gold market by certain bullion banks. The plaintiff was a contributor to GATA's study on the gold market, Gold Derivative Banking Crisis, which is posted at its website (www.gata.org) and has been downloaded in full PDF format more than 20,000 times. The plaintiff was also a member of the GATA delegation that met with the Hon. Dennis L. Hastert, Speaker of the U.S. House Representatives, in May 2000 to present to him the conclusions of the GATA study. Much of the evidence cited in this complaint comes from GATA's many friends and supporters worldwide.

4. The defendant Bank for International Settlements ("BIS"), frequently described as "the central banks' central bank," describes itself as an international organization but has not been so designated under the International Organizations Immunities Act, 22 U.S.C. s. 288 et seq. The BIS is headquartered at CH-4002 Basle, Switzerland. Its principal owners and customers are the central banks of the major industrial nations. The BIS accepts gold deposits, makes gold loans, holds approximately 200 metric tonnes of gold for its own account, and is an active participant in the gold market. Its manager responsible for foreign exchange and gold, Giancomo Panizzutti, received the "Man of the Year Award" from the COMEX at its annual gold dinner in New York recently. Under the auspices of the BIS, gold derivatives (along with foreign exchange, interest rate, equity and other derivatives) are subject to significant regulation and reporting, including: (1) the Basle Capital Accord, which sets minimum bank capital adequacy requirements for off-balance sheet derivatives; and (2) protocols for disclosure of information regarding derivatives, both in the financial statements of individual firms and through reports prepared by national regulatory authorities as well as by the BIS from country data submitted to it.

5. The defendant Alan Greenspan is Chairman of the Board of Governors of the U.S. Federal Reserve System ("Fed"), 20th Street and Constitution Avenue, NW, Washington, D.C. 20551. Mr. Greenspan has served ex officio as a director of the BIS continuously since September 1994. When the BIS was formed in 1930, 15% of its original capital -- the so-called American issue or tranche -- was subscribed publicly in the United States, thereby giving the Fed the right to vote these shares when, as and if it assumed the two seats allocated to the American issue on the BIS's board. However, by a public pronouncement issued May 15, 1929, Secretary of State Henry L. Stimson forbade "any officials of the Federal Reserve system either to themselves serve or to select American representatives as members of the proposed International Bank." In fact, the two American seats on the BIS's board remained vacant until July 1994, when Mr. Greenspan, without any formal authorization by Congress, the President or the Secretary of State, acted to assume them for the Fed. Since September 1994, the Fed's two nominees have participated fully in the affairs of the BIS and voted the shares of the American issue.

6. The defendant William J. McDonough is President of the Federal Reserve Bank of New York ("N.Y. Fed"), 33 Liberty Street, New York, New York 10045. Mr. McDonough has served as a director of the BIS continuously since September 1994, occupying the second seat allocated to the American issue under the BIS's original plan of organization. As of August 2000, approximately 7127 metric tonnes of "earmarked" gold belonging to foreign official institutions, mostly central banks, were held in custody accounts at the N.Y. Fed, down from 8621 tonnes at the end of 1995. At the end of 1999, the N.Y. Fed held gold certificates covering over 40% of the total U.S. gold stock, far more than any other Federal Reserve Bank, and up from 30% ten years previously.

7. The defendant J.P. Morgan & Co. Inc. ("Morgan") is a global financial services firm with its head office at 60 Wall Street, New York, New York 10260, and a usual place of business at 2 International Place, Boston, Massachusetts. Morgan is a major international bullion bank. Its wholly-owned commercial bank subsidiary, Morgan Guaranty Trust, is required to provide regular quarterly reports on its gold derivatives to the U.S. Controller of the Currency ("OCC"). As of June 2000, Morgan reported US$29.7 billion notional amount of gold derivatives, up from $18.4 billion one year earlier.

8. The defendant Chase Manhattan Corp. ("Chase") is a bank holding company with its head office at 270 Park Avenue, New York, New York 10017, and a usual place of business at 101 Federal Street, Boston, Massachusetts. Chase is a major international bullion bank and recently often a heavy seller of gold on the COMEX. Its wholly-owned commercial bank subsidiary, Chase Manhattan Bank, is required to provide regular quarterly reports on its gold derivatives to the OCC. As of June 2000, Chase reported US$35 billion notional amount of gold derivatives, up from $20.5 billion one year earlier.

9. The defendant Citigroup, Inc. is a diversified financial services holding company with its head office at 153 East 53rd Street, New York, New York 10043, and a usual place of business at 1 International Place, Boston, Massachusetts. Citibank N.A. ("Citibank"), Citigroup's wholly-owned commercial bank subsidiary, is a major international bullion bank, and is required to provide regular quarterly reports on its gold derivatives to the OCC. As of June 2000, Citibank reported US$11.4 billion notional amount of gold derivatives, up from $7.2 billion one year earlier. Together, Morgan, Chase and Citibank accounted for about 83% of all gold derivatives reported to the OCC in June 2000, and 75% one year earlier. In combined notional amount, the gold derivatives of these three banks increased by over $30 billion, or by over 65%, during this one year period while those of all other reporting U.S. commercial banks remained virtually flat at slightly over $15 billion.

10. The defendant Goldman Sachs Group, Inc. ("Goldman") is a global investment banking and securities firm with its head office at 85 Broad Street, New York, New York 10004, and a usual place of business at 125 High Street, Boston, Massachusetts. Goldman is a major international bullion bank and recently often a heavy seller of gold on the COMEX. Goldman is generally regarded as a major purveyor of gold derivatives. However, not being a commercial bank, Goldman does not report its gold derivatives to the OCC.

11. The defendant Deutsche Bank AG ("Deutsche Bank") is an international bank with its head office at Taunusanlage 12, D-60262, Frankfurt am Main, Germany, and a usual place of business at One Federal Street, Boston, Massachusetts. Deutsche Bank is a major international bullion bank and recently often a heavy seller of gold on the COMEX. In June 1999 Deutsche Bank acquired Bankers Trust, a U.S. commercial bank which itself had a significant gold derivatives business. In its 1999 annual report, Deutsche Bank reported approximately US$51.2 billion notional amount of gold derivatives at year-end, up from $16.2 billion one year earlier. Most of this increase came in the last half of the year.

12. The defendant Lawrence H. Summers is the Secretary of the Treasury. Pursuant to 31 U.S.C. s. 5302, the Secretary of Treasury has exclusive control of the Exchange Stabilization Fund ("ESF") subject only to the approval of the President. The ESF and the Fed are the only instrumentalities of the federal government with broad statutory authority to trade in gold. This authority was conferred at a time when the dollar was officially defined by Congress as a specified weight of gold, and when maintenance of the dollar's official gold value was a matter of substantial legal and practical concern. Public financial statements of the ESF provide evidence of its intervention in the gold market, particularly since 1998.

13. Collectively the defendants represent all the principal parties required for a just and complete adjudication of the price fixing claims. The publicly reported gold derivatives of two other major international banks engaged in this business, UBS AG and Credit Suisse Group, do not show the same extraordinary growth patterns over the past two years as the gold derivatives of the defendant bullion banks, nor have these two Swiss-based banks recently been reported as frequent heavy sellers of gold on the COMEX. An examination of the gold hedging activities of the world's two largest gold mining companies, AngloGold Ltd. based in South Africa and Barrick Gold Corp. based in Canada, suggests that both companies have material non-public knowledge of the gold price fixing scheme which they have used to their advantage, but neither company appears to play a critical role in implementing the scheme.

14. The plaintiff purchased his BIS shares, which then traded over-the-counter in Basle but now trade on the Swiss Exchange, in 1989 through an American brokerage firm. The shares were held in street name until 1997, when the plaintiff registered them in his name on the books of the BIS and soon thereafter received share certificate no. 031419 inscribed to him at his U.S. address, where the certificate remains. The plaintiff purchased his 1200 depositary shares of Gold-Denominated Preferred Stock, Series II, of Freeport-McMoran Copper & Gold, Inc., at various times from 1995 through 1999. By its terms, each depositary share pays a quarterly cash dividend equal to the value of 0.0008125 ounce of gold and will be redeemed in February 2006 for the cash value of 0.1 ounce of gold. The quarterly dividends are cumulative, but to date all payments have been timely made based on the arithmetic average of the London PM gold price over the relevant preceding five-day period.

15. By a "Note to Private Shareholders" dated September 15, 2000, mailed to the plaintiff at his U.S. address, the BIS gave notice that its board planned to vote at a meeting on January 8, 2001, to compel all private holders of the American, Belgian and French issues to surrender their shares against a payment of SwF16,000 (approx. US$9280) per share notwithstanding an opinion from J.P. Morgan & Cie SA, a wholly-owned French-based subsidiary of Morgan, setting the per share net asset value at US$19,099, or more than twice what the BIS proposes to pay for the shares that it plans to take.

16. Venue is based on 28 U.S.C. s. 1391(b)(2) as to all defendants, s. 1391(c) with respect to the corporate defendants having usual places of business in Boston, Massachusetts, s. 1391(d) with respect to the BIS and Deutsche Bank, and s. 1391(e)(2) and (3) with respect to Messrs. Greenspan, McDonough and Summers, all of whom are acting "under color of [federal] legal authority" with respect to the matters alleged notwithstanding that their conduct falls wholly outside their legal and constitutional authority. Venue of the claims under the Exchange Act is also based on s. 27 thereof, 15 U.S.C. s. 78aa. Venue of the claims under the Sherman Act is also based on s. 12 of the Clayton Act, 15 U.S.C. s. 22, as to the corporate defendants.

III. Development of Today's Gold Market 17. From 1792 to the closure of the gold window in August 1971, gold functioned in an official monetary role under the Constitution and laws of the Unites States. Gold's use in ordinary domestic coinage ended in 1934 with the monetary measures of the New Deal, including the devaluation of the dollar from $20.67/ounce to $35/ounce and a general prohibition on the ownership of gold by United States citizens. Under the Bretton Woods Agreements (59 Stat. 512 (1945)) adopted after World War II, gold remained at the center of the international monetary system and the United States committed itself to redeeming dollars presented by official foreign monetary institutions at the legal standard of $35/ounce. When the United States unilaterally ceased redeeming dollars for gold in August 1971, the Bretton Woods system collapsed. Since then, the international payments system has moved to floating exchange rates with no currency convertible into gold at fixed parities. The Second Amendment to the Articles of the International Monetary Fund ("IMF"), adopted under U.S. pressure in 1978, further limits the use of gold for official monetary purposes.

18. In 1972, Congress authorized and directed the Secretary of the Treasury to establish a new par value for the dollar of $38/ounce (Pub. L. 92-268, s. 2, 86 Stat. 116 (1972)), which it amended in 1973 to $42.22/ounce or 0.828948 IMF Special Drawing Right. Pub. L. 93-110, s. 1, 87 Stat. 352 (1973). Effective April 1, 1978, Congress repealed the 1973 par value act, leaving the dollar for the first time since 1792 statutorily undefined with reference to gold or silver. Pub. L. 94-564, s. 6, 90 Stat. 2661 (1976), repealing 31 U.S.C. s. 449. See 31 U.S.C. ss. 314, 821, repealed by Pub. L. 97-258, s. 5, 96 Stat. 877 (1982).

19. In 1974, Congress eliminated the restrictions that it had adopted forty years earlier on private ownership of gold by American citizens. Shortly thereafter trading of gold contracts was resumed on the COMEX. In 1977, Congress repealed the prohibition on gold clauses in private contracts, enabling the issue of gold-linked securities. Under the Gold Bullion Coin Act of 1985 (31 U.S.C. s. 5112, as amended by Pub. L. 99-185, 99 Stat. 1177), Congress authorized the United States to resume issuing gold coins having a legal tender face value but to be sold to the public at a price equal to the market value of the bullion at the time of sale plus costs of minting and distribution.

20. By its actions described in paragraphs 18-19 above, Congress effectively relegated gold to the status of an ordinary commodity for purposes of federal law, leaving its value against the dollar to be determined by market forces and without intervention by the Treasury, the ESF or the Fed, none of whom were given any legislative guidance whatsoever with respect to any particular price or price level for gold.

21. Although gold is now an ordinary commodity under federal law, it retains its intrinsic character as permanent, international money. Many of the world's nations, and most of its central banks, continue to hold significant quantities of gold as a part of their international monetary reserves. Of the estimated approximately 120,000 metric tonnes of above-ground world gold stocks, some 32,000 tonnes are currently claimed as reserves by official monetary institutions. (One metric tonne equals 32,150.7 troy ounces.) After the U.S. dollar, gold is the second largest component of official international monetary reserves. In addition, its price is widely regarded as an important economic indicator, particularly as a measure of U.S. inflationary pressures and the international strength of the dollar.

22. Because of its intrinsic character as money and its availability in quantity, gold functions in today's international markets as a stateless currency. Like any major currency, gold is not only borrowed and loaned at interest, but also arbitraged in spot and forward markets against other currencies on the basis of relative interest rates. Although gold interest rates are generally referred to as "lease" rates, the term is technically a misnomer. Gold is borrowed to be spent and repaid like a currency, not rented to be used and returned like a house or a car.

23. Since they were delinked, the dollar and gold have developed different interest rate structures. Lease rates on gold generally run at significantly lower levels than dollar interest rates, creating a situation of "contango" in gold futures, meaning that the dollar prices of gold for future delivery are higher than the spot price for current delivery. (The opposite of contango is "backwardation," meaning that spot prices are higher than futures prices.) Against the dollar, the contango on gold expressed as a percentage is roughly the U.S. Treasury bill rate less the lease rate. For gold to go into backwardation, this number would have to turn negative, i.e., the lease rate would have to exceed the Treasury bill rate.

24. Unlike other commodities where situations of contango and backwardation often result from varying expectations about future versus current supply, contango or backwardation in gold -- as in currencies -- is governed by relative interest rates since ordinarily neither gold nor currencies are subject to significant constraints with regard to current versus future supply. Currencies can be printed at virtually no cost by their issuing authorities. Gold, because it is produced for accumulation rather than consumption, is unique among commodities in that nearly all the gold ever produced remains in above-ground stocks, including the approximately 32,000 metric tonnes in official reserves.

25. Gold is traded internationally on a 24-hour basis in both physical and paper forms, with major markets in London, New York, Hong Kong, Tokyo, Zurich and Dubai. However, from the perspective of price discovery, the most important markets are the London Bullion Market Association ("LBMA") and the COMEX. Historically, the London market has been by far the largest in terms of volume or turnover. It does significant business in both bullion and paper instruments, but lacks transparency. The COMEX does relatively little business in physical gold, being principally a futures and options market. Zurich and Dubai are major physical markets. Most gold derivatives are traded over-the-counter between or among bullion banks, other financial institutions, gold mining companies, hedge funds, speculators and others. Unlike gold derivatives traded in standardized form as futures or options on exchanges such as the COMEX, over-the-counter gold derivatives are private contracts specially tailored to the requirements of the parties.

26. Annual new mine production of gold in 1999 was approximately 2500 metric tonnes, about the same as in 1998 and as estimated for 2000. At the same time, annual gold demand is running at over 4000 tonnes. Notwithstanding the annual excess of demand over supply, gold prices are well below the total cost of production for most mines. These low prices have forced closure of several, including the historic Homestake mine in Lead, South Dakota, high-grading in many others, and numerous job losses. Indeed, general conditions in the gold mining industry are the worst they have been since the 1960's. The deficit between new mine supply and demand, which has been growing steadily during the period covered by this complaint, has been met by scrap recovery, by some sales of official gold, and most importantly, by leased gold mostly from central banks.

27. Central banks lease gold either by making gold deposits with, or by making gold loans to, bullion banks, the largest of which are major international banks or other financial institutions. In both cases, the gold is placed with a bullion bank usually at a very low rate of interest, often 2% or less. This so-called "leased" gold is then sold into the market and the currency proceeds delivered for investment or other use by the bullion bank and/or its customer. When the gold deposit is called or the gold loan comes due, the physical gold required for repayment must generally be repurchased in the market. But during the term of the deposit or loan, the central bank retains the leased gold as an asset on its books and as part of its official gold reserves notwithstanding that the buyer of the leased gold owns it free and clear. The obligation to repay this gold to the central bank puts the bullion bank and/or its customer in a short physical position, i.e., they owe physical gold that they do not have.

28. This short position creates a risk to the borrower that when the loan comes due, the gold required for repayment may not be available in the market at prices at or below those at which it was sold. To mitigate this risk, gold borrowers typically hedge their exposure through the purchase of forward contracts or call options, which in turn are usually hedged by their purveyors, creating a complex web of derivative instruments.

29. Bullion banks, acting as agent or principal, are usually on both sides of these transactions. When acting as agent, their customers include gold producers (mining companies), fabricators (e.g., jewelry manufacturers), investors, traders and speculators. Gold producers often borrow gold through their bullion banks and sell it forward in order to earn the contango on some portion of their future production as well as to gain a measure of protection against falling prices. They may then make repayment by delivering gold from new production. Investors, traders and speculators often take advantage of gold's low lease rates to fund higher-yielding investments through the so-called gold carry trade. In addition, major banks sometimes borrow gold through their treasury departments for purposes of general funding.

30. Most central banks do not disclose the amount of gold that they have on lease. Bullion banks are even more secretive about the amounts of gold that they have borrowed. Accordingly, the current size of the aggregate short physical position is a subject of considerable controversy. Informed estimates range from 5000 to well over 10,000 metric tonnes, or several years of annual production. In April 2000 at a conference in Australia, Dinsa Mehta, head of global commodities trading for Chase, suggested a possible total short position of around 7000 tonnes, an amount that a recent report from Salomon Smith Barney describes as "simply too large to ever be repaid."

31. Gold derivatives, like other over-the-counter derivatives, are generally measured by their notional values, which are the face or reference amounts from which derivative payments are determined. Notional value is similar in concept to open interest, but measures it by face value of contracts instead of their number. Although a tiny portion of all derivatives, gold derivatives are very large in relation to physical gold supplies. Converted at the 1999 year-end gold price of about $290/ounce, the total market value of the world's roughly 120,000 metric tonnes of above-ground gold is $1.1 trillion, official gold reserves amount to almost $300 billion, and annual new mine production is a little over $23 billion. At the end of 1999, the BIS reported $243 billion total notional amount of gold derivatives, which converted at the same year-end price amounts to some 26,000 metric tonnes, ten times annual new mine supply and almost as large as total official reserves. As of June 30, 2000, the BIS reported that the total notional amount of gold derivatives had grown to $262 billion, or by 8%, notwithstanding falling gold prices during the period.

32. The gold derivatives of certain bullion banks, particularly Morgan and Chase, are also quite large in relation to their capital. For example, at the end of 1999, Morgan reported total risk-based capital of $12.1 billion and gold derivatives having a total notional value of over $38 billion, equivalent to roughly 3600 to 4000 metric tonnes of gold. On a position of this size and assuming an equal split between long and short contracts, should a swift upward move in gold prices to $600/ounce result in 20% of its counterparties being unable to deliver, Morgan could quite possibly suffer losses amounting to as much as 10% of notional value, or $3.8 billion, nearly a third of its capital.

33. Today prudential rules developed over centuries of experience with gold banking under earlier monetary regimes are ignored. Formerly bullion reserves of 40% against short-term gold liabilities were usually required. But today, no physical gold reserves are generally required or maintained. Gold derivatives may give theoretical protection against gold price risk, but they can neither replace physical gold when demanded nor substitute for it as a financial asset without credit risk, i.e., one that is not another's liability. Aimed at reducing firm risk, gold derivatives have instead created massive systemic risk in the precise area where the role of the lender of last resort is inherently limited -- gold banking. The Fed cannot print gold to rescue either the bullion banks or other banks that have used the gold carry trade as a source of apparently cheap funding. What it can do, for a while at least and contrary to law, is actively to assist and support manipulation of gold prices so that rising prices do not result in the short positions of the bullion banks causing them crippling and possibly fatal losses.

IV. Manipulation of Gold Prices 34. This complaint alleges manipulation of gold prices from 1994 to the present time by a conspiracy of public officials and major bullion banks. This manipulative scheme appears directed at three objectives: (1) to prevent rising gold prices from sounding a warning on U.S. inflation; (2) to prevent rising gold prices from signaling weakness in the international value of the dollar; and (3) to prevent banks and others who have funded themselves by borrowing gold at low interest rates and are thus short physical gold from suffering huge losses as a consequence of rising gold prices.

35. Support for the price fixing allegations in this complaint comes from various sources, including: (1) official reports of the BIS, OCC, Fed and ESF; (2) analyses of market data; (3) statements by certain participants in the manipulative scheme; and (4) statements by others with knowledge of the manipulative scheme.

36. The basic model for the manipulation appears to be the London Gold Pool, which operated without formal agreement under the auspices of the BIS from 1961 to 1968. However, the present scheme differs in three critical respects: (1) it aims to subvert the free market price of gold rather than to defend an official price sanctioned by formal international agreement; (2) leasing rather than outright sales is the preferred method of bringing central bank gold to market; and (3) gold derivatives, built on a foundation of leased gold, are a new and important tool giving the manipulators a high degree of leverage.

37. While using gold derivatives to force down prices whenever possible, the manipulators must also find or coerce sufficient supplies of gold bullion to meet strong physical demand, particularly from Asia, responding in part to the low prices resulting from their own manipulations.

38. In July 1998, Fed Chairman Alan Greenspan, testifying before the House Banking Committee, stated: "Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise." This statement amounted to a declaration that the gold price had been and would continue to be controlled. Not only did it constitute an open invitation to take advantage of the gold carry trade at very little risk, but also it pressured private holders of gold bullion to sell or lease their gold, thus augmenting the physical supply needed by the manipulators.

39. In a formal letter to Senator Joseph I. Lieberman dated January 19, 2000, Mr. Greenspan elaborated on his 1998 congressional testmony: "This observation simply describes the limited capacity of private parties to influence the gold market by restricting the supply of gold, given the observed willingness of some foreign central banks -- not the Federal Reserve -- to lease gold in response to price increases." Thus the Fed chairman himself has admitted that some central banks lease gold not to earn a return on it as they often claim, but primarily to supply physical gold to the bullion banks during periods when strong demand is pushing up prices.

40. Table 3.13 in the monthly Federal Reserve Bulletin shows month-end balances of total foreign earmarked gold held at Federal Reserve Banks, virtually all of which is kept at the N.Y. Fed. Foreign earmarked gold decreased from 8865 metric tons at the beginning of 1995 to 7318 tonnes at the end of 1999, or by almost 1550 tonnes. While some of this decline may represent official sales rather than leasing, in general over this period surges in outflows from the N.Y. Fed coincided with periods of strength in gold prices. Mr. Greenspan's congressional testimony in July 1998 also corresponded with the first appearance of a noticeable slowdown in withdrawals of foreign earmarked gold from the N.Y. Fed in the face of rising gold prices.

41. According to reliable reports received by the plaintiff, the IMF is now leasing gold through the BIS. As an international financial institution, the IMF qualifies to use the banking facilities of the BIS. Although the IMF claims neither to lease gold nor to have legal authority to do so, a gold deposit made by the IMF to its account at the BIS might arguably be distinguished from a gold loan. Such a deposit would, however, provide physical gold for lease by the BIS. In its most recent annual report for the year ending March 31, 2000, the BIS disclosed that during the year gold deposits by central banks fell almost 12% from 927 metric tonnes to 819 tonnes, and that gold held in bars declined almost 20% from 813 tonnes to 658 tonnes. At the same time, the BIS's total gold lending increased 47 tonnes to 360 tonnes, almost double the level of 185 tonnes as of March 31, 1996.

42. The IMF holds over 3200 metric tonnes of gold. American and British officials tried to tap this supply for manipulative purposes in 1999 through the proposed sale of over 300 tonnes ostensibly to fund aid to heavily indebted poor countries, an initiative that received strong support from both the Clinton administration and the Blair government. On May 7, 1999, just as gold threatened to surge over $300/ounce in response to new doubts whether the proposed IMF gold sales would go forward, the British announced that the Bank of England, on behalf of the Exchange Equalisation Account in the British Treasury, would sell 415 tonnes of gold in a series of public auctions. Although this announcement came with no warning and was completely unexpected by most, the previous evening Bill Murphy of GATA reported in his Midas column at Le Metropole Cafe: "Deutsche Bank's bullion desk is calling their clients saying that the gold market is stopping at $290."

43. Various British officials have offered wholly unpersuasive explanations of these auctions as an effort to diversify Britain's international monetary reserves. But British gold reserves were already low compared to those of other major European nations. British officials have not agreed on who made the decision. However, the timing virtually guarantees not only that it came directly from the prime minister, but also that he must have had extraordinary reasons for making it. His government was a leading supporter of the proposed IMF gold sales. The announcement clumsily put Britain in the position of front-running the IMF, ultimately a significant factor in forcing it to change tack. The manner of the British sales -- periodic public auctions in which the entire lot is sold at the lowest price accepted for any portion -- is so inconsistent with obtaining the best available return for British taxpayers that it has triggered an inquiry by Britain's National Audit Office.

44. Intertwined connections of present and former government officials and high ranking executives of the bullion banks and certain major gold mining companies have facilitated the conspiracy to manipulate gold prices. These connections include but are not limited to: Robert E. Rubin, former U.S. treasury secretary, previously co-head of Goldman and now a top executive at Citigroup; Frank B. Arisman, managing director of gold operations at Morgan and a director of AngloGold; Vernon E. Jordan, presidential confidante and a member of Barrick Gold's international advisory board; and E. Gerald Corrigan, former N.Y. Fed president and now a managing director at Goldman.

45. Many of the most egregious manipulative activities have occurred on the COMEX, which has high international visibility, but being predominantly a paper market, is more easily subject to manipulation. Over the past two years, Goldman, Chase and Deutsche Bank have regularly appeared as heavy sellers of gold on the COMEX whenever necessary to kill any significant rally. In the past year, many observers of the gold market have noticed a tendency for gold prices to rise in overseas trading only to be knocked back to prior levels on the resumption of trading in New York. Recently, amidst volatility in many other markets caused in part by a disputed presidential election in the United States, gold settled on the COMEX for 21 straight trading days within $1 of $266/ounce.

46. Among the more rigorous analyses of the gold market is an article by Michael Bolser entitled "Anomalous Selling in COMEX Gold, 1985 to November 2000" recently published at The Golden Sextant. Mr. Bolser identifies six extreme episodes of very heavy or "preemptive selling" in COMEX gold since 1994. For this purpose, preemptive selling is defined as the COMEX closing price falling by more than three times the decline in the London PM fix from the AM fix on the same day. In other words, if the AM fix is $300 and the PM fix is $295, the COMEX price would have to fall by more than $15 to less than $280 in order for the day to register as one with preemptive selling. For each month, the days with preemptive selling are taken as a percentage of the total trading days, and the percentages for each month are then charted.

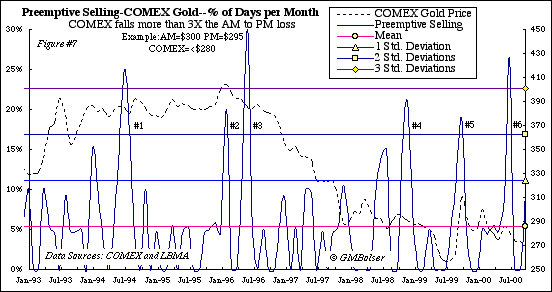

47. Although defined solely on a statistical basis, each period of extreme preemptive selling coincides with a period when gold prices displayed marked weakness in circumstances where historical trading patterns called for just the opposite behavior. Although the manipulative scheme has operated on a daily or as needed basis to control and subdue gold prices, analysis of these six periods of extreme preemptive selling illustrates the operation of the scheme.

48. Since January 1985, there have been only seven episodes of preemptive gold selling on the COMEX in excess of two standard deviations from the mean, of which only three have exceeded three standard deviations. Of these seven episodes, all but one have occurred since January 1994. These six are shown graphically as waves 1 through 6 on Figure #7 below, which is taken from Mr. Bolser's addendum.

49. The only other preemptive gold selling in excess of two standard deviations occurred very briefly in early 1985. It was followed in late 1986 by a longer period of heavy preemptive selling not quite reaching the level of two standard deviations. This 1986 episode, which took place as gold prices moved sharply higher while the Iran-Contra affair unfolded, is the longest sustained high level of preemptive selling until 1994. It corresponds with the most significant activity of the ESF in the gold market prior to 1999 as revealed by tables 1.18 and 3.12 in the relevant monthly Federal Reserve Bulletins. (See paragraphs 62-63.)

50. The first wave of preemptive selling in excess of three standard deviations occurred in mid-1994, coincident with Mr. Greenspan's decision to assume the two seats on the BIS's board allocated to the American issue. Gold prices, which had been in a generally rising mode for the prior year and a half, went into an extended sideways move that lasted until 1996. The OCC reports on gold derivatives only go back to the first quarter of 1996, at the end of which the total notional amount of gold derivatives held by reporting U.S. commercial banks stood at $57.6 billion. Thus by mid-1994 it is probable that American bullion banks had already established a short position in physical gold of sufficient size and risk to concern the Fed.

51. The second and third waves of preemptive selling took place in 1996. At the beginning of the year, there was an episode (wave 2) in excess of two standard deviations, followed in mid-1996 by an episode (wave 3) in excess of three standard deviations. The first took place as gold threatened to push significantly over $400/ounce. The second started gold prices on a long downward course to under $300 by late 1997. According to reliable reports received by the plaintiff, the Fed was telling certain persons in early 1996 that gold would not pass $415/ounce. At the same time, the near zero interest rate policy adopted by Japan in mid-1995 to try to address its deepening financial problems was impacting the gold market in three ways: yen gold prices on the Tokyo Commodities Exchange were moving into backwardation; dollar gold prices were rising; and lease rates were climbing, suggesting strong demand for physical gold.

52. Noting "the extraordinary rise in gold lease rates" at the end of 1995, the BIS in its 66th annual report cited "gold lenders follow[ing] their usual practice of reducing their credit exposures at end-year," explaining that "those who needed to borrow gold to sell it short had to offer unusual compensation." A story headlined "Sharp Rise in Gold Lease Rates Revives Market" in The Wall Street Journal on December 5, 1995, reported that lease rates had fallen back the prior two days as "central banks and other investors made more metal available,...in part because of persuasion from the Bank of England, the unofficial custodian of the world's bullion market." At the annual gold roundtable of The Wall Street Transcript in December 1995, not one of the six analysts present expressed any serious worry over negative effects on gold prices from unusually high central bank gold sales or gold loans in 1996. However, by the end of 1996, the gold price was in rapid descent, falling to around $345/oz. in early 1997, and touching well below $300 by the end of that year.

53. The fourth wave of preemptive selling in excess of two standard deviations, occurred with the collapse of Long-Term Capital Management ("LTCM") during the Russian default crisis of October 1998. According to reliable reports received by the plaintiff, LTCM had funded itself using the gold carry trade and was short 300 to 400 metric tonnes of gold at the time of its collapse. To prevent the covering of this short position from driving gold prices higher, the N.Y. Fed arranged an off-market transaction, probably involving Chase. It is similarly reported that the principals of LTCM received some form of immunity or accomodation on condition that they not reveal or discuss LTCM's short gold position.

54. On September 26, 1999, fifteen European central banks, with the European Central Bank, Banque de France and Bundesbank in key leadership roles, announced without prior warning an agreement to limit their gold sales and not to expand further their gold lending. Unveiled in Washington, D.C., after the annual meetings of the IMF and World Bank, this agreement is generally referred to as the Washington Agreement. According to most European press reports, the agreement was prepared in secrecy and without the knowledge of American, British or BIS officials, although the Bank of England was given and accepted an opportunity to sign onto the agreement just before the announcement. The Washington Agreement triggered an explosive rally in gold prices.

55. The fifth wave of preemptive selling in excess of two standard deviations occurred in response to this rally as the Fed, the Bank of England and the BIS struggled to halt and reverse it. According to reliable reports received by the plaintiff, this effort was later described by Edward A. J. George, Governor of the Bank of England and a director of the BIS, to Nicholas J. Morrell, Chief Executive of Lonmin Plc:

We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it. It was very difficult to get the gold price under control but we have now succeeded. The U.S. Fed was very active in getting the gold price down. So was the U.K.

56. A major consequence of the gold rally following the Washinton Agreement was the near bankruptcy of Ashanti Goldfields Ltd., a large gold mining company based in Ghana, due to huge paper losses from hedging strategies devised for it by Goldman apparently on the assumption that gold prices could not rally as they did. Goldman's actions with respect to Ashanti were the subject of scathing comment, including allegations of serious conflicts of interest, in an article by L. Barber and G. O'Connor, "How Goldman Sachs Helped Ruin and then Dismember Ashanti Gold," Financial Times (London), Dec. 2, 1999. The principal shareholders of Ashanti, which is listed on the New York Stock Exchange, are Lonmin and the Government of Ghana.

57. The following table shows the total notional amount of gold derivatives, all maturities, of Chase, Morgan, Citibank and Other as reported by the OCC from December 1998 through June 2000. All amounts are in US$ billions. (Columns do not add due to rounding and exclusion of separately stated figures for Bankers Trust prior to June 1999.) The largest relative and absolute increases are highlighted in bold.

Bank 12/98 3/99 6/99 9/99 12/99 3/00 6/00 Chase 24.1 23.7 20.5 22.6 22.1 31.5 35.0 Morgan 16.8 15.1 18.4 30.5 38.1 36.3 29.7 Citibank 6.7 7.3 7.2 10.7 11.8 11.8 11.4 Other 15.0 13.5 14.2 19.3 15.7 15.9 15.7 Total 68.3 65.1 61.4 83.3 87.6 95.5 92.158. In the foregoing table, the figures for 9/99 are as of September 30. Accordingly, they reflect positions as of four trading days after announcement of the Washington Agreement. During these four days the gold price moved from about $265/ounce to over $300. The rally continued into October, with gold prices trading as high as $325 during the first two weeks, and then generally declining to just under $300 by the end of the month. For the rest of 1999 and into February 2000, gold traded in a $20 dollar band under $300. In the second week of February, a sharp rally took gold to over $315, but again the price was quickly brought under control, and it remained generally in the $280-290 range from the beginning of March through June, although falling into the low $270's in May.

59. In January 2000, Barrick Gold revealed that following the Washington Agreement it had purchased call options covering 6.8 million ounces of gold, or over 210 metric tonnes, to protect itself against possible losses on its forward contracts in 2000 and 2001. According to reliable reports received by the plaintiff, these call options were purchased from Morgan, which has offices in Toronto in the same building as and one floor above Barrick Gold's. The risk of selling call options in this volume to a company possessing the power to take unilateral actions that could drive gold prices much higher suggests that the underlying motive and purpose of this transaction must have been market manipulation.

60. The sixth and most recent wave of preemptive selling, this time in excess of three standard deviations, occurred in mid-2000, driving gold prices from $290/ounce to below $270. Canadian Imperial Bank of Commerce ("CIBC"), which apparently has assumed overall responsibility from Goldman for managing Ashanti's hedge book, is advising Ashanti regarding sale of a 50% interest in its Geita gold project in Tanzania to AngloGold. This transaction, which became unconditional on November 30, 2000, and is expected to close by December 15, required the approval of Ashanti's bullion banks and its shareholders, including Lonmin and the Government of Ghana. According to reliable reports received by the plaintiff, representatives of CIBC held discussions with Fed officials while this transaction was pending. In the course of these discussions, Mr. Greenspan's desire to hold down gold prices was expressed. Ashanti's financial problems presented a major risk not only to its survival but also to the balance sheets of its bullion banks.

61. Goldman recently recommended three gold mining stocks: AngloGold, Barrick Gold and Placer Dome, Inc. The first two, as noted in paragraph 13 above, are heavy hedgers who appear to have material non-public knowledge of the gold price manipulation scheme. According to reliable reports received by the plaintiff, Chase intimidated Placer Dome, also a heavy hedger, into denying that it had contributed to GATA when it in fact had. All three of these companies, although making announcements about reducing their hedge books in the wake of the Washington Agreement, have since returned to active hedging programs, including the writing of call options on gold, a sure sign that they do not expect any repetition soon of the fall 1999 gold rally.

62. The published financial statements of the ESF indicate that it has participated in the gold price fixing scheme along with the Fed. The monthly Federal Reserve Bulletins contain a table 1.18 showing end-of-month balances in the Fed's gold certificate account and a table 3.12 showing end of month balances in the total U.S. gold stock, including the ESF. The quarterly U.S. Treasury Bulletins also contain a table IFS-1 showing the U.S. gold stock, which states in footnote 2: "The Treasury values its gold stock at $42.2222 per fine troy ounce and pursuant to 31 United States Code 5117(b) issues gold cerificates to the Federal Reserve at the same rate against all gold held." Accordingly, any difference between the end-of-month figures reported in tables 1.18 and 3.12 reflects gold held or owed by the ESF.

63. From 1974 through 1985, end-of-year (December) balances in tables 1.18 and 3.12 matched precisely except for 1978, when there was a minor difference of $1 million ($11,718 million in the gold certificate account and $11,719 million in the account including the ESF). At the end of 1986, there was $20 million less, equal to almost 15 metric tonnes at $42.2222/ounce, in the account including the ESF than in the gold certificate account. Examination of the month-end figures reveals the following differences when subtracting the account including the ESF from the gold certificate account: October 1986, $18 million; November 1986, $14 million; December 1986, $20 million; and January 1987, $13 million. In February 1987, the account including the ESF exceeded the gold certificate account by $26 million, and in March 1987 the two accounts were brought back into balance. The preemptive selling in 1986 thus coincided with a unique period in which the ESF appears to have borrowed from the U.S. gold stock to sell bullion into the market, later replacing its gold borrowings with purchased bullion.

64. Tables 1.18 and 3.12 remained in balance on a year-end basis from 1987 through 1995 except for 1988 and 1991, when at year-end the account including the ESF was less than the gold certificate account by $3 million and $2 million, respectively. However, beginning in December 1996, tables 1.18 and 3.12 show a pattern of increasing discrepancies between the Fed's gold certificate account and the account including the ESF. The latter exceeded the gold certificate account by $1 million at year-end 1996 and $3 million at year-end 1997. However, the account including the ESF was $1 million less than the gold certificate account at the end of November 1997. At year-end 1998, the account including the ESF was $5 million less than the gold certificate account, but had been $1 million more at the end of the previous May. For the first time since 1986, there was a series of small monthly discrepancies between the two accounts in the first half of 1999, after which they remained in balance until year-end, when the account including the ESF showed a record $41 million, or approximately 30 metric tonnes, excess over the gold certificate account ($11,089 million versus $11,048 million). In January 2000 the two accounts were brought back into balance at $11,046 million.

65. These discrepancies between the Fed's gold certificate account and the account including the ESF strongly point to losses on gold trading, probably incurred primarily through some form of participation in gold derivatives, as the reason for the ESF's recent poor trading results. The ESF's profits or losses (-) on foreign exchange (the account that historically included gold) by fiscal quarter for 1997 through March 2000, as reported in table ESF-2 of the relevant quarterly U.S. Treasury Bulletins, are shown below. All amounts are in US$ millions.

Fiscal Oct./ Jan./ Apr./ Jul./ Total Year Dec. Mar. Jun. Sep. FY 2000 -1627 -394 1999 1699 -817 -500 1257 1637 1998 -754 -333 -135 576 -646 1997 -383 -1093 402 -538 -161366. While the Asian financial crisis might explain the ESF's losses in 1997, the Clinton administration reported to Congress that it did not engage in any currency interventions from 1998 through March 2000. During this period, the ESF's profits generally coincided with periods of falling gold prices while its losses coincided with rising gold prices. Its third largest quarterly loss ever occurred in the last calendar quarter of 1999, coincident with the explosion in gold derivatives on the books of Morgan, Chase, Citibank and Deutsche Bank. However, the ESF achieved excellent trading results in the prior calendar quarter dominated by falling gold prices resulting from the May 1999 announcement of British gold sales.

V. BIS's Proposed Freeze Out of Private Shareholders 67. By a "Note to Private Shareholders" dated September 15, 2000, the BIS gave notice that its board planned to vote at a meeting on January 8, 2001, to compel all private holders of the American, Belgian and French issues to surrender their shares against a payment of SwF16,000 (approx. US$9280) per share. In the same note, the BIS stated that it had received an opinion from J.P. Morgan & Cie SA, a wholly-owned French-based subsidiary of Morgan, setting the per share net asset value at US$19,099.

68. According to the BIS's note, 72,648 shares comprising 13.73% of its total capitalization are held by private shareholders, including all 33,078 shares of the American issue. The remaining shares are owned by central banks, but the Fed owns none. In 1999, the BIS issued a total of 12,000 new shares to several new central bank members, including the European Central Bank, at a price of 5020 gold francs per share, payable in gold or an equivalent amount in a currency acceptable to the BIS based on the market price of gold at the date of payment.

69. Article 20 of the BIS's Statutes provides: "The operations of the Bank for its own account shall only be carried out in currencies which in the opinion of the Board satisfy the practical requirements of the gold or gold exchange standard." Since its opening in 1930, the BIS has used the Swiss gold franc of that date as its unit of account, making conversions against various currencies as appropriate at market or historic rates against gold. Both the BIS's profit and loss statements and its balance sheets are published in gold francs. The gold franc is defined under Article 4 of its Statutes as 0.29032258 grams fine gold, and is indicated on its financial statements by a "GF" prefix.

70. The GF5020 per share price on the new shares issued in 1999 equals 1457.317 grams, or 46.8538 troy ounces, which at US$280/ounce equals $13,119, more than the amount that the BIS is proposing to pay its private shareholders but less than the net asset value per share assigned by Morgan. In stating the freeze-out price for its private shareholders in current Swiss francs rather than gold francs, the BIS violated both its statutes and all its prior practices, particularly with respect to transactions on capital account.

71. The principal justifications given by the BIS and Morgan for discounting the freeze-out price to less than half of net asset value are that private shareholders do not have voting rights and their shares have low trading liquidity. No BIS shares have voting rights. The right to vote pertains to each member central bank (or approved proxy therefor) based on the number of shares allocated to, and taken down under, that bank's non-fungible issue without regard to whether ownership of the shares rests with the central bank or in private hands. All original shareholders, whether private persons or central banks, paid in exactly the same amount of gold per issued share. The right to vote was not then, and has not since, ever been given a value, let alone a value in derogation of the full property value of the shares. The effort to compare the BIS to a corporation in which there are two classes of shares, voting and non-voting, is without any foundation in the Statutes of the BIS or its prior practices.

72. The liquidity argument is similarly bogus. No mention or consideration is given to the observed fact that the liquidity of the Belgian and French issues is much lower than that of the American issue. If liquidity were a valid consideration, the discount applied to the Belgian and French issues would be greater than that applied to the American issue, and holders of the American issue would receive a higher price. What is more, there are many steps that the BIS could take, particularly in cooperation with its member central banks or other financial institutions, to increase the market liquidity of its privately held shares, including the issuance of public certificates against these shares as authorized under Article 16 of its Statutes.

73. Describing the rationale for the freeze-out, the BIS states: "This measure is intended to enable the BIS to pursue better its objectives of promoting international monetary and financial cooperation." Further on, the note continues:

Indeed, unlike a commercial bank, the prime objective of the BIS is to employ its resources in support of its public interest functions. ... The existence of a small number of private shareholders, whose interest is essentially financial, is no longer seen to be in line with the international role and future development of the organisation. The BIS is, moreover, the only international organisation in the monetary and financial field to have private shareholders (in contrast to the IMF, the World Bank and the OECD).

74. As the note itself admits, the BIS is unique in having private shareholders whereas the IMF and the World Bank, both created in the wake of World War II, do not. However, the United States joined both of these Bretton Woods organizations pursuant to treaties presented by the President and approved by the Senate. What is more, U.S. contributions to both organizations required appropriations approved by Congress.

75. The United States was not a party to the Convention establishing the BIS. Participation of the Federal Reserve in the BIS rests solely on its dual public/private nature and the private shares originally subscribed in the United States. A major reason for this unique structure is that when the BIS was formed amidst the isolationist atmosphere of 1929-30, it was assumed that Congress would neither approve the Convention nor authorize a subscription of shares by the Fed. In fact, the Secretary of State expressly forbade the Fed to participate either directly or indirectly in the BIS, and neither Congress nor the President has ever taken any official action with respect to the United States joining the BIS or participating in its affairs.

76. The BIS's note fails to give the precise language of the several amendments proposed to implement the freeze-out. However, the note does affirm that "... shares withdrawn from private shareholders will not be cancelled, but will be redistributed among central bank shareholders of the BIS on 8 January 2001 in the manner determined by the EGM." This language suggests that some undisclosed proposal for redistributing the shares must already exist. Unless the American issue is to be purchased by the Fed, there will be no basis for its continued voting or participation in affairs of the BIS. However, since the Fed is not presently a shareholder, it does not qualify as a potential distributee under a literal reading of the language quoted.

77. In addition to their capital contributions, the private shareholders are responsible for three important attributes of the BIS: (1) creating plausible justification for some minimal level of American participation through the Fed or, in its absence, some acceptable private American financial institution; (2) requiring that the BIS's operations meet general standards of fiduciary duty to ordinary shareholders, including the pursuit of sound banking practices and publication of audited financial reports; and (3) providing the potential sanction of private shareholder actions should the BIS, under the direction of its central bank members or through the collusion of some, operate in a manner that violates its Statutes.

78. A basic guiding principle of the BIS is set forth in Article 19 of its Statutes, which states: "The operations of the Bank shall be in conformity with the monetary policy of the central banks of the countries concerned." As Henry H. Schloss in The Bank for International Settlements (North-Holland Publishing Co., Amsterdam, 1958) points out (p. 41): "This provision was important in allaying fears of those who objected to an international superpower which could destroy a country's sovereignty."

Count 1 (Price Fixing) 79. This count runs against all defendants, and incorporates by reference all the allegations of part IV, paragraphs 34-66.

80. The manipulative activities of the defendants in the gold market constitute horizontal price fixing and are illegal per se as set forth by the Supreme Court in United States v. Socony-Vacuum Oil Co., 310 U.S. 150, 223-224 (1940):

Under the Sherman Act a combination formed for the purpose and with the effect of raising, depressing, fixing, pegging, or stabilizing the price of a commodity in interstate or foreign commerce is illegal per se. ... Where the means for price-fixing are purchases or sales of the commodity in a market operation..., such power may be found to exist though the combination does not control a substantial part of the commodity. In such a case that power may be established if as a result of market conditions, the resources available to the combinations, the timing and the strategic placement of orders and the like, effective means are at hand to accomplish the desired objective. But there may be effective influence over the market though the group in question does not control it. Price-fixing agreements may have utility to members of the group though the power possessed or exerted falls far short of domination and control. ... Proof that a combination was formed for the purpose of fixing prices and that it caused them to be fixed or contributed to that result is proof of the completion of a price-fixing conspiracy under s. 1 of the Act.

81. Mr. Justice Douglas, who wrote this opinion of the Court, described perfectly the current international gold price fixing cartel a half century before its time. The defendants, through an intentional and coordinated scheme involving the use of gold derivatives when possible and leased official gold when necessary, have conspired to restrain gold prices and to prevent them from rising to the levels that would otherwise prevail in a free market. This scheme has been carried out on various world gold markets, including but not limited to the COMEX, through orchestrated sales in needed amounts at critical times and price levels.

82. This price fixing conspiracy involves an unholy alliance of certain high public officials and large bullion banks. The former have participated in order to camouflage and mitigate their own public policy failures, and specifically to prevent rising gold prices from: (1) signaling a warning of future U.S. inflation; (2) affecting the international standing of the U.S. dollar; (3) calling further attention to huge and unprecedented U.S. trade deficits; (4) impeding the inflows of foreign capital necessary to offset these large trade deficits; (5) causing political embarrassment to the Clinton administration and its claims of economic success; and (6) inflicting severe financial losses on favored banks and other financial institutions that have funded themselves using the gold carry trade.

83. Through their participation in the price fixing conspiracy, the defendant bullion banks have made many hundreds of millions of dollars while assisting their political friends, who have done whatever they can to protect the bullion banks from the risks of their short positions in physical gold as well as from any effective form of legal sanction.

Count 2 (Securities Fraud) 84. This count runs against the BIS, Alan Greenspan, William J. McDonough and Morgan (collectively the "BIS defendants"), and incorporates by reference all the allegations of count 1 plus part V, paragraphs 67-78.

85. The BIS defendants are persons within the meaning of the Exchange Act. Section 10(b) thereof and Rule 10b-5 promulgated thereunder make it unlawful for any person in connection with the purchase or sale of any security, whether or not listed in the United States, by use the mails or any other instrumentality of interstate commerce: (a) to employ any device, scheme or artifice to defraud; (b) to make any untrue or misleading representation, whether by affirmation or omission, as to a material fact; or (c) to engage in any practice that operates as a fraud or deceit.

86. As set forth in Count 1, the BIS defendants have acted jointly and in concert with the other defendants to manipulate gold prices to lower levels than would otherwise have prevailed. Although central banks are major holders of gold, their real power comes from their issuance and control of paper currencies. When they try to enhance their reputations by manipulating gold prices in today's free market, they damage all investments that closely correlate with the price of gold, including the value of BIS shares.

87. Historically there is a high correlation between gold prices and market prices on the Swiss Exchange for BIS shares. This correlation, which continued to manifest itself in the wake of the Washington Agreement, rests in part on the approximately 200 tonnes of physical gold that the BIS holds for its own account. Although the percentage of the share price directly attributable to its own gold holdings has declined as its other reserves have grown, there remain over 12 ounces of gold per share, equal to around $3400/share at $280/ounce gold. Additionally, as described in paragraphs 69-70, since the BIS maintains its books in gold francs, the gold price acts directly on its accounts, affecting any calculation of net asset value. Because the price of gold directly impacts both the market value and the net asset value of its shares, any actions by the BIS aimed at depressing gold prices operate in direct opposition to the interests of its private shareholders.

88. With full knowledge of the manipulative activities in the gold market and with specific intent to defraud the BIS's private shareholders, including the plaintiff, the BIS defendants have sought to take advantage of artificially and illegally depressed gold prices to freeze-out the BIS's private shareholders at a grossly unfair and inadequate share price. In furtherance of this fraudulent scheme, Morgan prepared a valuation opinion at the request of the BIS specifically for use in connection with the freeze-out. As a participant in the gold price fixing conspiracy and with full knowledge thereof, Morgan had to know that its valuation opinion could and would be used to perpetrate a fraud.

89. The BIS defendants have knowingly and intentionally failed to disclose material facts, and knowingly and intentionally made false and misleading statements of material facts, with respect to the manipulation of gold prices, including but not limited to: (1) the leasing of gold by central banks for the specific purpose of halting increases in gold prices; (2) the manner and means of handling LTCM's large short position in gold at the time of its collapse; (3) the true reasons for the British gold auctions; (4) the efforts of the Fed and the Bank of England to "quell" and "manage" the gold price after the Washington Agreement; (5) the manner and means by which gold reserves of the IMF are currently being employed in an effort to restrain gold prices; (6) the role played by the ESF in manipulating gold prices; and (7) the official support being given to Morgan, Chase, Deutsche Bank and perhaps other bullion banks to enable them to maintain and enlarge their huge volumes of gold derivatives.

90. The total notional amount of gold derivatives reported by Morgan, Chase and Citibank at June 30, 2000, converted to metric tonnes at $280/ounce, amounts to 8461 tonnes, slightly more than the total official gold reserves of the United States. The year-end 1999 gold derivatives of Deutsche Bank converted at the year-end gold price of $290/ounce amount to roughly 5000 metric tonnes, or some 1500 tonnes more than Germany's official gold reserves. Gold derivatives positions of these magnitudes concentrated in four banks are simply too large and too risky to represent normal business done in ordinary course.

91. The BIS defendants have knowingly and intentionally failed to disclose material facts, and knowingly and intentionally made false and misleading statements of material facts, with respect to other matters relevant to the proposed freeze-out of the BIS's private shareholders, including but not limited to: (1) the critical role of gold prices in determining the value of BIS shares; (2) the unprecedented practice of trying to ascribe or assign a monetary value to voting rights in the BIS; (3) the issuance of new shares to the European Central Bank and other central banks in 1999 at a price substantially in excess of the proposed freeze-out price; (4) the proposed redistribution of the private shares to central banks already holding shares, including to which banks and at what prices these shares are to be distributed; and (5) the effect that withdrawal of the American issue will have on the Fed's participation in the BIS in view of the fact that it is not a shareholder.

Count 3 (Common Law Fraud and Breach of Fiduciary Duty) 92. This count runs against the BIS, Alan Greenspan, William J. McDonough and Morgan, and incorporates by reference all the allegations of counts 1 and 2.

93. Quite apart from the provisions of the Exchange Act, count 2 sets forth a claim for common law fraud. The fraudulent scheme, which is extensive, blatant and intentional, also involves clear and knowing violations of law, including the Sherman Act, the Constitution, and Articles 19 and 20 of the Statutes of the BIS, by all the BIS defendants. Accordingly, punitive damages are fully warranted against each.

94. The BIS, Alan Greenspan and William J. McDonough have also breached their fiduciary duty to the plaintiff by issuing new shares in the BIS at less than full net asset value. Whatever argument might be made in favor of issuing a few shares at low prices to new central banks to encourage them to join the BIS, a nominal amount of shares would be sufficient for this purpose. Issuing more than a nominal amount of shares to the European Central Bank, which is basically an association of major central banks that are already members of the BIS, or to other central banks constitutes unwarranted and unjustified dilution.

Count 4 (Constitutional Violations) 95. This count runs against the BIS, Alan Greenspan, William J. McDonough and Lawrence H. Summers, Secretary of the Treasury, and incorporates by reference all prior allegations in so far as relevant.

96. Since 1994, Alan Greenspan and William J. McDonough have served as directors of the BIS, assuming the two seats on its board allocated to the American issue. So far as can be determined from the public record, neither of them has been authorized so to serve by Congress, the President or the Secretary of State.

97. The monetary provisions of the Constitution grant to Congress sole and exclusive power to determine the gold value of the dollar. "The Congress shall have power ... To coin Money, regulate the Value thereof, and of foreign coin." U.S. Const., Art. 1, s. 8, cl. 5. "No State shall ... coin Money; emit Bills of Credit; make any Thing but gold and Silver Coin a Tender in Payment of Debts." U.S. Const., Art. 1, s. 10, cl. 1. The Supreme Court has refused to decide whether Congress may constitutionally sever any meaningful link between the dollar and gold or silver, i.e., whether the U.S. monetary system in place since the closing of the gold window in 1971 is constitutional. But quite apart from this issue, if there is to be a link between the dollar and gold, the Constitution vests in Congress exclusive power to define it. This determination does not and cannot rest in the uncontrolled discretion of the Fed or the ESF, particularly when that discretion is exercised in secret and away from public view.

98. In his letter of January 19, 2000, to Senator Lieberman, Fed Chairman Greenspan conceded: "Most importantly, the Federal Reserve is in complete agreement with the proposition that any such transactions on our part, aimed at manipulating the price of gold or otherwise interfering in the free trade of gold, would be wholly inappropriate." Similarly, various officials working under the Secretary of Treasury, but not Secretary Summers himself, have purported to deny that the ESF has intervened in the gold market. Although these denials do not reflect the truth, they do reflect actual knowledge that any such interventions would be and are illegal and unconstitutional.

99. Because the Fed cannot conduct any monetary policy that violates the Constitution or laws of the United States, neither can the BIS when the Fed, with or without proper U.S. authorization, is a participant in its activities. Coordinating the London Gold Pool from 1961 to 1968 to maintain official gold parities established by law and international treaty is one thing. Recreating a similar operation in today's free gold market is quite another, particularly when that operation is used as a means to circumvent the Constitution and thus also constitutes a violation by the BIS of Article 19 of its Statutes.

100. These four defendants have conspired in a scheme which is directed, among other things, at taking the plaintiff's six shares of the American issue of the BIS without paying him fair value therefor or granting him due process of law in connection therewith.

Relief Requested Wherefore, the plaintiff requests the following relief:

(1) A permanent injunction enjoining Alan Greenspan, William J. McDonough, their subordinates and their successors in office, and the Secretary of the Treasury, acting through the Exchange Stabilization Fund or otherwise, from intervening in the gold market, directly or indirectly, for the purpose of affecting or with intent to affect gold prices;

(2) A permanent injunction enjoining J.P. Morgan & Co. Inc., Chase Manhattan Corp., Citigroup, Inc., Goldman Sachs Group, Inc., and Deutsche Bank AG, or any of their officers, employees, agents or subsidiaries, from manipulating or trying to manipulate gold prices, directly or indirectly, on the Commodities Exchange in New York or elsewhere;

(3) An order directing Alan Greenspan and William J. McDonough to resign forthwith as directors of the Bank for International Settlements, to withdraw their designations of alternates to serve in their absence, and to refrain from any further participation in its affairs or activities;

(4) An order directing the Bank for International Settlements to redeem and cancel all shares of its American issue, including the six shares owned by the plaintiff, paying for each share in gold an amount equal to its net asset value in gold francs, plus an appropriate amount for goodwill;

(5) An award of damages to compensate for the decrease in the gold franc value of the plaintiff's shares of the American issue of the Bank for International Settlements resulting from the illegal manipulation of gold prices by the defendants;

(6) An award of damages to compensate for the decreased dividend payments received by the plaintiff on his depositary shares of Gold-Denominated Preferred Stock, Series II, of Freeport-McMoran Copper & Gold, Inc., resulting from the illegal manipulation of gold prices by the defendants;

(7) An award of treble damages, costs and attorneys' fees on the plaintiff's price fixing claims;

(8) An award of punitive damages on the plaintiff's common law fraud and breach of fiduciary duty claims;

(9) Such other relief as the Court may deem appropriate.

Demand for Jury Trial The plaintiff demands trial by jury for all issues so triable.

By the plaintiff, /s/ Reginald H. Howe ________________________ Reginald H. Howe, Pro Se e-mail: row@ix.netcom.comDecember 7, 2000